The Hunt For Debt Financing In Canada

OVERVIEW – Information on debt financing in Canada . From short term loans to revolving credit facilities Canadian entrepreneurs and business people seek finance solutions that will work for their needs

Debt financing in Canada , whether it’s short term loans, asset financing, and other traditional and alternative finance forms requires some solid understanding of who’s involved and what’s involved. Let’s dig in.

Business owners and financial managers feel a lot more comfortable taking on debt ( versus raising equity ) when they understand they have negotiating ability while at the same time recognizing that are terms and other requirements that come with debt.

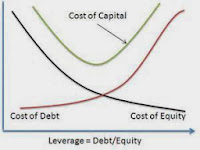

As we have noted debt is the opposite of your other form of capital – that’s equity of course. While no one form of financing is all perfect all the time debt finance via short term loans, etc has significant advantages. The bottom line on that is, of course, that using debt properly allows the owner /manager to grow the company with appropriate leverage.

And that’s without giving up the ownership you forsake in considering equity dilution.

When looking at a debt solution one other advantage is that there is always and end in sight via repayment, cash flow assessment, etc – again our bottom line is you can plan on retiring debt a lot more easier than equity takeouts.

One solid way for the business owner/financial manager to look at debt asset finance solutions is to assess them from the point of view of restrictions – i.e. what they can and can’t do by utilizing the covenants and ration requirements that come with any single form of debt – for example a senior term loan with a bank.

We’re big supporters of hybrid type solutions; one good example is asset based lines of credit that may or may not contain a term loan component. While you do take on ‘ debt ‘ at the same time you have corresponding assets such as inventory, equipt. and receivables that offset the entire obligation. Some owners might even agree to a small equity component to a debt deal that makes sense for their business. In corporate terms this is known as a warrant / option, etc.

While debt financing can be secured or unsecured. Whatever the case it’s always going to come down to your cash flow – historical, present, and thank god… projected! That cash flow will often be the key component in the bank or commercial finance company’s decision to grant business credit. If debt is unsecured we can only say that the ownership/management better be able to prove good credit quality. Unfortunately unsecured debt typically is only being achieved by firms with great combinations of cash flow, clean balance sheets and healthy profits.

Canadian firms who can accurately demonstrate and project sales, asset quality, and turnover of current assets are always in a better position to take on any form of business debt. The lender will of course make their own assumptions on the quality of your overall business credit situation.

If we had to identify one mistake our clients often made it’s that they chased the wrong financing sources for the type of debt or asset monetization they really need. Talk about a false start

in business that’s both expensive and time consuming.

If you want to isolate the identify the types of debt financing via short term loans or other methods of business finance seek out and speak to a trusted, credible and experienced Canadian business financing advisor who can assist you with your finance needs.

Author: Stan Prokop – founder of 7 Park Avenue Financial

http://www.7parkavenuefinancial.com

Originating business financing for Canadian companies, specializing in working capital, cash flow, and asset based financing. In business 10 years – has completed in excess of 90 Million $$ of financing for Canadian corporations. Core competencies include receivables financing, asset based lending, working capital, equipment finance, franchise finance and tax credit financing.

Info re: Canadian business financing & contact details:

CONTACT:

Greg LaBella

7 Park Avenue Financial

Off. 905 829 2653

Cell 905 302 4171